Summary

Manulife Insurance Review 2025

Executive Summary

Verdict: For cross‑border HNW cases—especially trust‑owned or premium‑financed—Manulife’s international platforms combine top‑quartile financial strength with flexible UL/IUL mechanics and robust Asia hub access. This review distils what matters for planners and families making high‑stakes, multi‑jurisdictional decisions.

For HNW clients, you’ll find an independent view you can read directly or discuss with your financial adviser.

For financial advisers, Capital for Life’s proprietary scoring and market research strengthen suitability notes, validate provider selection, and support compliant recommendations.

🔒 This article is a preview. The full 4,500‑word review—including our proprietary weighted scoring framework, suitability matrices, available solutions, jurisdiction notes and downloadable adviser tools, is available to Capital for Life members.

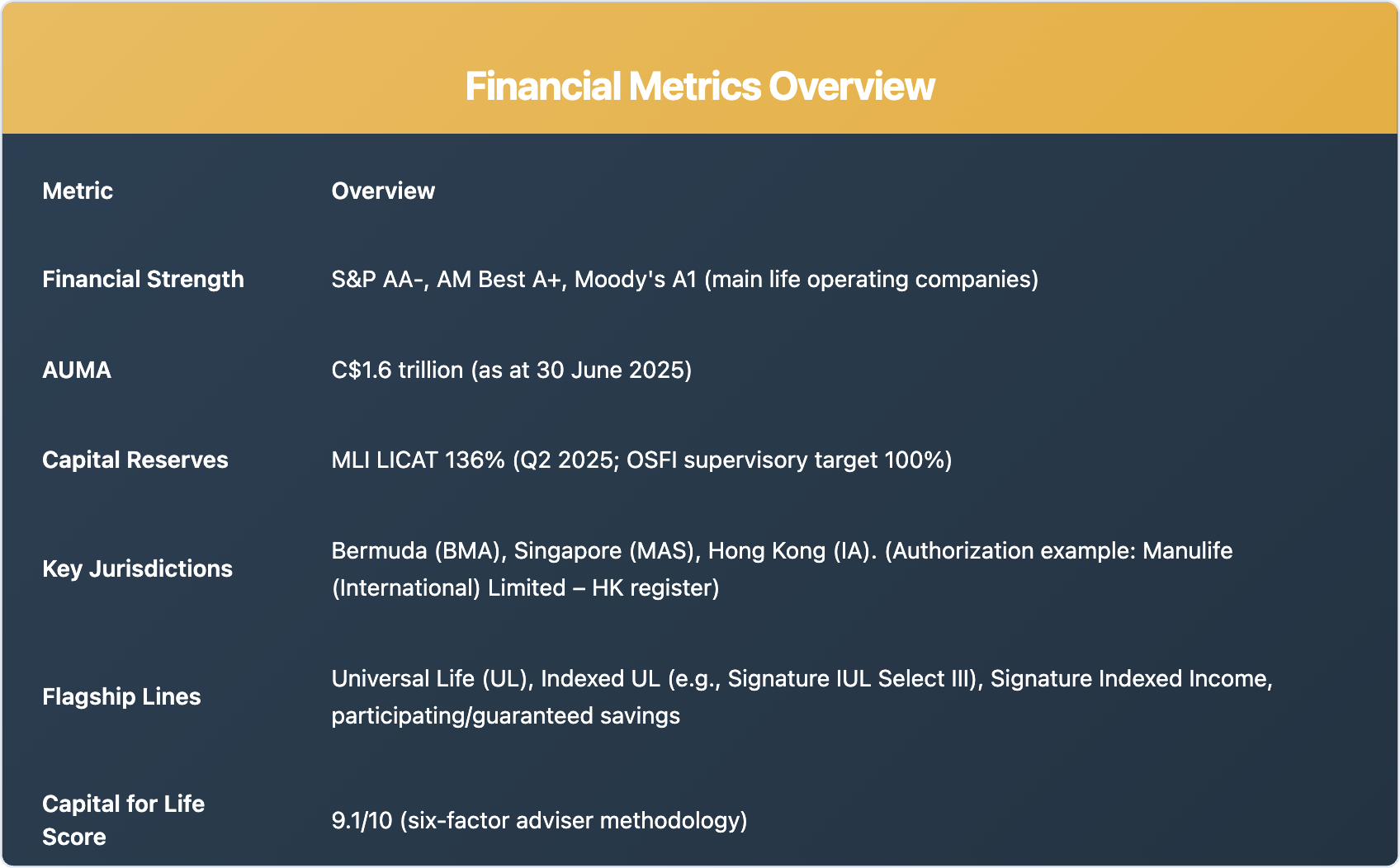

Manulife at a Glance (2025)

Manulife Financial Strength

Manulife’s scale (AUMA C$1.6T), strong ratings (S&P AA‑ / AM Best A+ / Moody’s A1), and MLI LICAT 136% underpin suitability for long‑duration policies, trust ownership, and bank premium financing. These metrics matter when policies are intended to last decades across multiple legal and tax regimes.

Global Structuring Access

Manulife supports international HNW clients through three hubs:

- Bermuda – common‑law flexibility for trust‑owned policies via The Manufacturers Life Insurance Company (Bermuda Branch); regulated by BMA.

- Singapore – onshore integration under MAS oversight; access to Signature series including IUL and income solutions.

- Hong Kong – Manulife (International) Limited authorised by the Insurance Authority; suited to Greater China families and multi‑currency portfolios.

Popular Manulife Solutions for Financial Advisers

- Indexed Universal Life (IUL) – Manulife Indexed Universal Life Insurance Pro, Manulife Global Indexed Universal Life Insurance 24 and Signature Indexed Universal Life Select (III) are all popular IUL solutions used for (U)HNW investors.

- Universal Life (UL) – e.g., Heirloom series for estate liquidity and legacy.

- Indexed Income / Savings – Signature Indexed Income links to the S&P 500 index mechanics with downside floor and flexibility for income planning.

- Term life – available in selected markets (e.g., Singapore: ManuProtect Term (II)).

Policy loans: Access to cash value is possible; loan rates are not guaranteed to be below crediting rates. Example: Manulife Singapore currently lists a 6.75% p.a. policy‑loan rate (subject to change). Always rely on the Product Summary/Illustration for current terms.

Innovation That Matters

- Downside protection & crediting mechanics: 0% floor for index crediting; cap/participation rates apply.

- Automatic Premium Spread (APS): Optional feature to smooth index allocations over time.

- Fixed Account floor: 2% p.a. minimum guaranteed (product‑specific; see SIULS III brochure).

- Streamlined/tele‑medical underwriting (where available) for executive‑level applicants.

- Quit Smoking Incentive: smokers may qualify for non‑smoker treatment initially, subject to program rules and medical evidence to keep the status. (Applies on selected plans, including Heirloom and ManuProtect Term (II).)

Methodology (Summary)

We rate international insurers for HNW planning across six factors:

1. Financial strength & capital (LICAT, ratings);

2. Product depth & competitiveness (UL/IUL/participating);

3. Underwriting & service (HNW readiness);

4.Jurisdictional access & portability;

5. Structuring/financing support (trust/TOLI, premium financing);

6. Adviser enablement (tools, documentation, SLAs).

(Weights and scorecards inside the Capital for Life members’ section.)

Who Manulife Best Serves

Best for

- HNW clients seeking USD policies, often with premium financing.

- Advisers working with trusts/family offices across multiple jurisdictions.

- Clients prioritising estate liquidity and legacy planning with global hub access.

Less suited

- Smaller, budget‑led needs with no cross‑border complexity.

- Clients seeking low‑sum assured (< ~US$2m) whole life solutions in isolation.

🔍 Want the Full 4,500‑Word 2025 Manulife Review?

This is an independent, adviser‑led assessment based on real cases, underwriting feedback, and our proprietary scoring framework. If you’re recommending or investing in Manulife, unlock the materials we use internally:

Capital for Life Members get

- Downloadable adviser tools + product research PDF

- Weighted scoring framework and jurisdictional matrices

- Premium‑financing lender notes (indicative LTV/collateral ranges)

- Copy‑ready tables, FAQs, and compliance‑friendly planning notes

👉 Unlock the full review to structure recommendations with confidence.

Join Capital for Life

Access the full review, templates, comparisons, and scorecards. Become a member to streamline cross‑border cases and document recommendations faster.

FAQs – Manulife Insurance Review 2025

Does Manulife offer Indexed Universal Life (IUL)?

Yes. Manulife offers Indexed Universal Life through platforms such as Singapore and Labuan. Products include Signature IUL Select (III), featuring a 0% floor, caps, participation rates, and optional Automatic Premium Spread.

Is term life available internationally from Manulife?

Yes. Term life is available in select jurisdictions—for example, ManuProtect Term (II) in Singapore. Availability depends on local regulations and client residency.

Is Manulife suitable for high-net-worth clients?

Manulife is suitable for high net worth clients. Manulife combines AA- financial strength, multi-jurisdictional platforms, and flexible IUL options, making it a preferred insurer for HNW planning, especially in trust, financing, or offshore contexts.

Can Manulife policies be used for retirement income?

Yes. IUL and Indexed Income plans allow policyholders to build tax-efficient cash value, which can be accessed via policy loans or withdrawals during retirement while preserving death benefit.

Can Manulife policies be held in offshore trusts?

Yes. Manulife’s international life products are often structured into offshore trusts for estate planning, wealth transfer, and asset protection, especially in Bermuda, Singapore, and Hong Kong.

What are Manulife’s main international hubs?

Manulife operates through Bermuda (BMA-regulated), Singapore (under MAS), and Hong Kong (IA-authorised). Each offers distinct benefits for trust ownership, regulatory treatment, and currency options.

Disclaimer

Authored by Carlton Crabbe, Chief Executive Officer, Capital for Life – a specialist life insurance agency focused on international HNW solutions.The information herein is general and not personal financial, legal, or tax advice. Product availability, terms, and suitability vary by jurisdiction and client profile. Manulife is a trademark of The Manufacturers Life Insurance Company. Consult qualified advisers before acting.

Manulife Insurance Review 2025 – HNW Product Insights

Read Case Study

Join the Capital For Life Advisor Hub

Access the complete 10-point checklist, stress-test worksheet, and client presentation slides inside the Capital for Life Membership Hub.

Become a Member Today